Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The process of buying a home can be overwhelming at times, but you don’t need to go through it alone. This free eGuide will answer many of your questions and likely bring up a few things you didn’t even know you should consider when buying a home!

The process of buying a home can be overwhelming at times, but you don’t need to go through it alone. This free eGuide will answer many of your questions and likely bring up a few things you didn’t even know you should consider when buying a home!

For a while now baby boomers have been blamed for a portion of the housing market’s current lack of housing inventory, but should they really be getting the blame?

Aaron Terrazas, Senior Economist at Zillow, says that “Boomers are healthier and working longer than previous generations, which means they aren’t yet ready to sell their homes.”

According to a study by Realtor.com, 85% of baby boomers indicated they were not planning to sell their homes.

It is true that baby boomers are healthier and are thus working and living longer, but are they also refusing to sell their homes?

Last month, Trulia looked at the housing situation of seniors (aged 65+) today compared to that of a decade ago. Trulia’s study revealed that:

“Although seniors appear to be delaying downsizinguntil later in life, as a group, households 65 and over are still downsizing at roughly the same rate as in years past.”

Trulia also explains that,

“5.5% of households 65 and over moved, pretty evenly split between moves to single family (2.7%) and multifamily (2.4%) homes. In 2005, these percentages were virtually the same, with 5.5% of senior households moving, including 2.5% into single family and 2.5% into multifamily homes.”

Recent reports tell us that the older population grew from 3 million in 1900 to 47.8 million in 2017.

In addition, the Census recently revised the numbers from their National Population Projections:

“The aging of baby boomers means that within just a couple decades, older people are projected to outnumber children for the first time in U.S. history…By 2035, there will be 78.0 million people 65 years and older compared to 76.7 million under the age of 18.”

If you are a baby boomer who is not sure whether you should downsize or move to a warmer climate (other people are doing it, why not you?), let’s get together so we can help you evaluate your options today!

It’s hard to imagine having to take care of your parents — and your kids — until it becomes a reality.

A lot of us don’t think about it, but not having a plan for your parents can affect more than just your heart: It can affect your wallet, too.

“Because these are emotionally charged topics with the involvement of money, the tendency of people is to avoid the conversation,” said Mark Hamrick, senior economic analyst at Bankrate.com. “That is a recipe for a bad outcome.”

Senior care is expensive. If your parents don’t have sufficient savings or health insurance or long-term care — you could be paying out of pocket to help them.

Researchers at the Center for Retirement Research estimated that if you take care of them yourself, you’ll likely spend 77 hours per month, which equates to an (unpaid) part-time job. Either way, it’s a doozy: The average hourly cost of home care is $21, which means it could cost more than $5,000 per month for daily 9-to-5 care.

Long-term care insurance prices vary, but you can count on the fact that they rise with age: If you wait to purchase, long-term care goes from an average of $2,978 for a couple at age 55 to $3,770 for a couple at age 60, according to the American Association for Long-Term Care Insurance.

And what if you have to pay for both an aging parent and a growing kid at the same time? If you do, you’re probably part of the sandwich generation (the group of us who are responsible for caring for both those younger than us and those older). According to Hamrick, they could both cost about the same — which is to say, they both cost a lot.

“It’s not unusual these days for a private university to cost $60,000 a year,” said Hamrick. “When you think about a nursing home costing several thousand dollars a month, we’re sort of in comparable territories there.”

Yikes. Ouch. Yeah. What do we do about this? I’m wondering the same thing.

Don’t worry, there are ways to prepare and get secured. We’re with you. These six steps can help:

If your parents are still healthy enough to take care of themselves, it’s important to sit down with them to review a full list of assets, accounts and incomes. Ask what they have saved for their retirement, where they want to live and what needs to be done in a medical emergency.

If they’re already in need of care, figure out what assets they have and what care is actually needed. You don’t want to pay for assisted living now, when they might only need occasional visits from an in-home care professional.

The best way to plan for your parents’ retirement, your kids’ college and your retirement, too, is by saving aggressively. Budgets are the best way to squirrel away some money, but once-in-a-while things like holiday bonuses can be used to save, too.

“People should keep these kinds of costs in mind when making their saving plans, realizing that there is a large probability that they may need to spend resources, time or money on elderly parents,” said Gal Wettstein, a research economist for the Center for Retirement Research at Boston College.

A long-term care insurance policy helps cover the costs of that care when you have a chronic medical condition, a disability or a disorder like Alzheimer’s disease. Most policies will reimburse you for care given in places like your home or a nursing home. You never know if you or your parents will need it, but just like any other kind of insurance, it can be a godsend in case something unexpected happens. Though this kind of insurance has gotten more expensive in recent years, it’s worth looking into when you or your parents are nearing 50.

Take full advantage of different accounts and programs that are available to you. If you’re qualified, you can open a health savings account for a parent, which allows you to put money aside tax-free for health costs — including the costs of premiums on policies like long-term care insurance.

For your children, 529 plans have huge tax education savings benefits: All withdrawals are tax-free and all gains are tax-deferred when used for expenses related to education. Same thing goes for Coverdell education savings accounts. One key difference is that Coverdells have a $2,000 yearly contribution limit, whereas 529 plans have limits in the hundreds of thousands (it varies by state). Another thing to keep in mind is that with Coverdells, once the student hits 18, the student controls the account. 529 plans may be a better option for your family if your child is known to overspend and you’d like to control the funds.

Alice Zulkarnain, another research economist for the Center for Retirement Research at Boston College, said that adults who take care of elderly parents tend to retire earlier, “before they intend to.”

“That missed labor income adds up to a large effect,” she added. In other words, that’s a lot of income they’ve lost out on — and, if they have primarily saved for retirement though 401(k)s, that’s money lost for their retirements, too.

That’s all the more reason to make sure your retirement savings are good to go. If your company matches on 401(k) contributions, take full advantage. You can also open a Roth IRA if your company doesn’t have a 401(k) option — or if you feel like saving a little more. Roth IRAs are great: You pay taxes upfront, which means the money you withdraw in old age is tax-free, so if you know you’ll retire in a higher tax bracket, they make great sense taxwise.

No matter what your finances look like during this time, it’s hard. We get it. And so do so many other ladies, especially those in the Working Daughter Facebook support group. If you need a little extra support, turning to women who will understand you is never a bad call. And remember, we’re here for you, too. Join the HerMoney Facebook group of like-minded ladies looking for more control and less chaos.

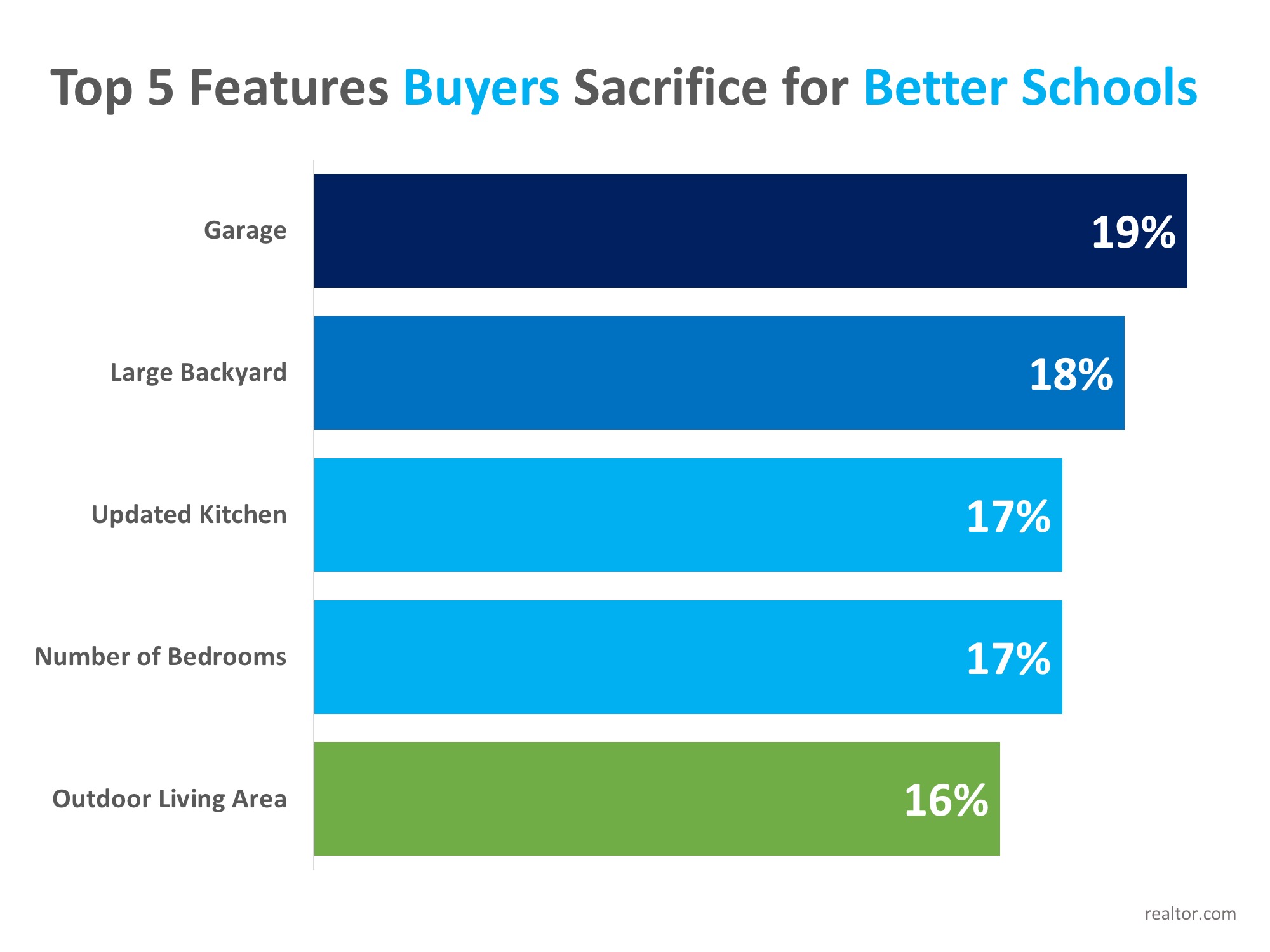

It should come as no surprise that buying a home in a good school district is important to homebuyers. According to a report from Realtor.com, 86% of 18-34 year-olds and 84% of those aged 35-54 indicated that their home search areas were defined by school district boundaries.

What is surprising, however, is that 78% of recent homebuyers sacrificed features from their “must-have” lists in order to find homes within their dream school districts.

The top feature sacrificed was a garage at 19%, followed closely by a large backyard, an updated kitchen, the desired number of bedrooms, and an outdoor living area. The full results are shown in the graph below.

Buyers are attracted to schools with high test scores, accelerated academic programs, art and music programs, diversity, and before and after-school programs.

With a limited number of homes available to buy in today’s real estate market, competition is fierce for homes in good school districts. Danielle Hale, Chief Economist for Realtor.com, explained further,

“Most buyers understand that they may not be able to find a home that covers every single item on their wish list, but our survey shows that school districts are an area where many buyers aren’t willing to compromise.

For many buyers and not just buyers with children, ‘location, location, location,’ means ‘schools, schools, schools.’” (emphasis added)

For buyers across the country, the quality of their children’s (or future children’s) education ranks highest on their must-have lists. Before you start the search for your next home, let’s get together to discuss the market conditions in our area.

Whether you’re casually browsing or currently trapped in the midst of a bidding war, no matter what stage of the home-buying or home-selling process you’re in, there will always be things you wished you had known beforehand. For any homeowner, the post-stress of buying or selling real estate comes down to the should haves, could haves, and would haves. Could I have put in a lower bid? Should I have considered other brokers? Wonder no more.

If you’ve ever wanted to get inside the mind of a real estate agent, now is your chance. From the do’s and don’ts of selling to how to negotiate like a pro, to what to know before you browse, we took some of your most pressing housing questions to the experts at Manhattan-based real estate firm Warburg Realty. Read on for everything they want you to know.

You love your stuff. And while we’re all for showing off your most precious possessions, that doesn’t mean the potential buyers coming to tour your space will feel the same. For sellers, staging your home can mean a lot of things, but it ultimately means creating a blank slate for future residents.

“It’s important to make the apartment look and feel as neutral as possible but give that sense that it feels like it can be lived in, even move-in ready if possible. Painting a fresh neutral color is a quick thing on the cheaper side that can always help,” Gannon Forrester, an agent at Warburg Realty, tells Domino.

Need help finding a suitable neutral paint? Here are our top 10 choices.

“While buyers may not decide to purchase a home within moments of entering, they most certainly decide not to buy it in those crucial first few minutes,” reveals Lisa Larson. “Staging to me means not just editing an overly cluttered apartment. It also means painting (which I consider the least expensive facelift you can give an apartment), removing and storing furniture, and bringing in new furniture and accessories.”

We get that you want the most bang for your buck, but don’t be unrealistic. Overpricing almost always discourages traffic and bids, and it’s one of the biggest reasons a beautiful home will sit on the market and go stale.

“For properties to sell in this market the price needs to be priced right from the beginning. After the initial burst of activity in the first two weeks or so, viewing request start to wane and at times there will be weeks without a call. If your home has not sold in the first few weeks, sellers should consider a meaningful price drop or risk the property languishing on the market for months,” suggests Larson.

The same sentiment rings true about getting a great offer right away. “The thing about sellers is if they get a great offer too soon, then they think it was underpriced. Before listing your property, calculate the net worth and make sure you are comfortable with the asking price,” explains listing agent Brandon Major.

Some agents will tell you that there isn’t necessarily a golden month or season to buy a home. And while it all really depends on where you live, there are certain times of the year when competition is low and those selling are more motivated to negotiate.

“Sellers who list in the summer are generally serious sellers and thus willing to consider all deals,” notes Larson. “School is set to begin in August or September and so no major life changes to cause a family to move are on the horizon. Therefore, summer is also a terrific time to shop.”

Some agents will tell you that there isn’t necessarily a golden month or season to buy a home. And while it all really depends on where you live, there are certain times of the year when competition is low and those selling are more motivated to negotiate.

“Sellers who list in the summer are generally serious sellers and thus willing to consider all deals,” notes Larson. “School is set to begin in August or September and so no major life changes to cause a family to move are on the horizon. Therefore, summer is also a terrific time to shop.”

Likewise, you might be more likely to snag your dream home for your dream price come the holidays. “I’ve done a lot of deals in December when everyone thinks it’s slow,” says Forrester. “Yes, there’s less inventory, but the apartments that are listed usually know what kind of market they are in and will be more willing to negotiate.”

“By doing this, your bid likely won’t match the bid of another party,” says Warburg agent Susan Abrams of one strong money strategy. Her other bidding tip? Make things personal!

If negotiating was as simple as calling up Drew Scott from the Property Brothersand having him handle all the haggling on your behalf, we’d all be doing it. Considering very few of us will ever have the chance to turn our HGTV dreams into a reality, we have to put in the extra elbow grease.

“Do your homework. Know the comparables for the property you are considering. Also, it’s important to understand the seller’s degree of motivation. Are they moving out of town for a new job or are they just testing the market? Assuming you’re dealing with a serious seller, make a bid that is not insulting, but based on real market data,” Larson tells Domino.

Really want to hurt your chances of negotiation? Putting an expiration date on an offer or counteroffer might seem like a solid strategy to get your seller to come down, but it often has the opposite effect.

“Buyers generally never walk away after the expiration date passes and sellers typically get annoyed by such a demand,” says Larson. “Sometimes just letting an offer sit says more than jumping in and demanding a response. A day or two of silence can work wonders.”

Case in point: Don’t play head games.

There might come a day when you’ll find yourself stuck in the middle of a bidding war. Want to come out on top? If you’re really looking to go all in, you might want to consider waiving your mortgage contingency, suggests Major. “Sellers love non-contingent offers, so waive that and your offer is as good as all cash, essentially,” he says.

Let the seller know that you’re serious about wanting the property. To avoid getting trapped in a back-and-forth bidding war be early, explains Larson. “Being the first to make a solid offer can give you an edge. And be thorough: A well-prepared offering package can be a leg up for buyers.”

If you’re the type of shopper who tends to go over budget no matter what you’re buying (shoes, groceries, a car, etc.), it’s important to give yourself parameters. “Ask yourself: What is the number I’m willing to go up to and be able to sleep at night knowing you would not have raised your bid even $10 higher?” says Larson.

Not to burst your bubble, but if you live in a city like New York, you’re going to have to put in a whole lot more effort to get your dream place. Before you even think about putting in an offer on a place, make sure you have all of your funding lined up, have an attorney, and get pre-approval for your mortgage.

“Being prepared also means having an understanding of the market. Many buyers will act on something based on the most recent article they read. A real estate market like NYC is a micro-market and many times people read about macro-trends. Nothing is worse than making a low ball offer based on old information and then losing out on the apartment you wanted,” shares Forrester.

Let’s get back to not being greedy. While it might feel tempting to decline an offer at full asking price that comes in right away, you can never be sure that another equally-great (or even better) offer is a guarantee.

“A client always wants an agent to sell the apartment as fast as possible, but when an offer comes in right away, this weird paradox occurs,” explains Forrester. “Instead of being happy many clients will start second-guessing things. Clients think that if one buyer comes along that quick, there will be several others just as interested, maybe even more interested. Months go by and when it sells, it was for a lower price than that first offer.”

Sure, you might only be casually looking now. But before you get serious about buying a home, you need to get serious about your broker.

“Meet for coffee and interview two to three buyer’s brokers and decide who you want to collaborate with on your home purchase,” suggests Abrams. “Properties featured online can be very deceptive and searching through all the online property options is time-consuming. A buyer’s broker can help you understand the options and make sure you don’t waste your time looking at the wrong homes for your needs.”

While a stellar view might not be a priority for every home buyer, it should rank higher on your must-have list or nice-to-have list than it currently does. Location, location, location, has as much to do with how close you are to the office and to shops and restaurants as it does with noisy streets and poor views. Two red flags you need to pay attention to when touring a space? The curtains are drawn and there’s music playing.

“Make sure the views and light are acceptable and that the music isn’t masking neighborhood noise. In general, look past the furniture and study the bones of the house. Come prepared with your list of must-haves but allow yourself to be open to some flaws. No house will check every single box,” shares Larson.

All moves are overwhelming. But downsizing can be especially challenging, as it often accompanies a major life change. Whether you’re simplifying, retiring, facing a freshly emptied nest, or making a move that will help you age in place, these tips from the Town & Shore team can help facilitate the process.

Size up your space. Take an honest look at which rooms you currently live in, and calculate how much square footage that amounts to. After your kids move out, you may find there are rooms or entire wings in the house that go unused. Also consider how lifestyle changes may impact how much house you require. If you’re moving from the suburbs to a city, for example, you may spend more time enjoying restaurants, and less time entertaining at home, eliminating the need for a formal dining room. Similarly, if you plan to use car services or public transportation, you may be able to sell one of your vehicles and get by with a single parking space.

Assess amenities. Think about what kinds of services you want, and what maintenance responsibilities you want to shed. Some people find gardening and yard work therapeutic, and couldn’t imagine giving them up. But if these chores are starting to feel unmanageable, you may want to move to a property where landscaping is taken care of. Other options to consider: Do you want access to a pool, gym, golf course, or tennis court? Do you want a concierge for security and to handle things like deliveries? All of these factors should play into your decision-making process.

Keep an open mind. Many people dismiss condo and high-rise living for fear they’ll lose their privacy. But you might discover that sharing walls connects you with people with whom you share common ground and provides a built-in support network. And remember — downsizing doesn’t mean downgrading. You can still have hardwood floors and a Viking range in a compact space. Tighter quarters can also change family dynamics for the better, as you’ll have more opportunities for togetherness with loved ones.

Address your stuff. Often, people are surprised to find that their kids don’t want furniture and dishes that have been in the family for generations. The owners know they have to pare down, but may not be ready to part with their precious items. Your real estate agent can help evaluate what your needs are and, if necessary, refer you to organizations that can facilitate the winnowing process. A downsizing specialist, for example, can help you decide what to keep and what to toss, and handle the logistics of getting items to antique dealers, auction houses, ebay, and charitable organizations.

Get the timing right. Lots of people try to time their sale to coincide with a peak in the market. But given the unpredictable nature of today’s real estate landscape, you’re better off moving when it makes sense for you. Carefully weigh the pluses and minuses of downsizing versus staying put. Talk it over with your loved ones. Make your life what you need today. Nobody knows what tomorrow will bring.

Mortgage interest rates, as reported by Freddie Mac, have increased by close to a quarter of a percent over the last several weeks. Freddie Mac, Fannie Mae, the Mortgage Bankers Association, and the National Association of Realtors are all calling for mortgage rates to rise another quarter of a percent by next year.

In addition to the predictions from the four major reporting agencies mentioned above, the Federal Open Market Committee recently voted “unanimously to approve a 1/4 percentage point increase in the primary credit rate to 2.75 percent.”Historically, an increase in the primary credit rate has translated to an overall jump in mortgage interest rates as well.

This has caused some purchasers to lament the fact that they may no longer be able to get a rate below 4%. However, we must realize that current rates are still at historic lows.

Here is a chart showing the average mortgage interest rate over the last several decades:

Though you may have missed the lowest mortgage rate ever offered, you can still get a better interest rate than your older brother or sister did ten years ago, a lower rate than your parents did twenty years ago, and a better rate than your grandparents did forty years ago.

October is here! Check out my latest issue of American Lifestyle at the link below:

http://digital.remindermedia.com/diane-terry/issue-92-vol-1/1/

When going from a 2,200-square-foot traditional home to a 300-square-foot renovated RV, my family and I ended up getting rid of 80 percent of our belongings. Downsizing is an experience that I recommend to anyone—no matter the size of your home. While living in a tiny vehicle might not be for everyone, I believe that getting rid of all that overwhelming “stuff” can help you live simpler and sometimes even happier.

When going from a 2,200-square-foot traditional home to a 300-square-foot renovated RV, my family and I ended up getting rid of 80 percent of our belongings. Downsizing is an experience that I recommend to anyone—no matter the size of your home. While living in a tiny vehicle might not be for everyone, I believe that getting rid of all that overwhelming “stuff” can help you live simpler and sometimes even happier.

If you’re looking to do a major purge, you could get instruction from an advice column or ask a “helpful” family member who is offering unsolicited opinions on things they haven’t been through in 30 years… Or, you could listen to me and my community of tiny dwellers—all who have shed the majority of their belongings somewhat recently. These six tips for simplifying your “stuff” from me, a tiny house dweller of more than a year, and others will help you prep for a successful purge, whether you’re downsizing from a house to an apartment, an apartment to a tiny house, or just trying to live more minimally.

My family has a rule that if we buy a new item—clothing, book, shoes, or toy for their kids—we must give an old item away. This prevents our downsized life from getting overcrowded.

We also limit our clothing items (under things excluded) to fifty items per family member, per season. We can also keep an off-season tote for things we find on sale for the next season or in the next size up for our kids without overloading their drawers or storage spaces.

“The first tip that was very useful for me was from a book called ‘Little House on a Small Planet,'” says Laura LaVoie, who lives in a 120-square-foot tiny house. “It suggested to put Post-It notes on the door to every room in your house. For a month or two, write down the reason for entering every time you go into a room. By the end of that time, look to see how you’re using your spaces. I found there were rooms in our large house I almost never used. That’ll give you an idea of how you really use spaces.”

When we downsized from our farmhouse with a playroom and individual rooms for each kid to our tiny home, we used square felt bins from a local department store to downsize toys. This gave our kids a visual and a better understanding that they had two bins each and if their stuff wouldn’t fit it couldn’t stay.

Sometimes you hold on to stuff because you think it has some larger meaning. “Books can make you feel smart if you have a lot of them on display, but books don’t make you smarter just by having them,” LaVoie says. “I started realizing that it was more productive to give away books I enjoyed to people who could also benefit from them.” If there is something you are sentimental about, that will serve a greater purpose in the hands of someone else, give it to another person to enjoy.

Carmen Shenk, known as “The Tiny House Foodie,” lives in a Skoolie conversion with her husband—their second tiny home. She recommends never forgetting the S.O.A.P:

Start small—but start. Even if it’s just going through that one shelf that’s been bothering you, a start to simplifying is still a start!

Only one right-sizing project at a time. Don’t jump into trying to downsize lots of things or many rooms at a time. This will likely cause you to become overwhelmed and unmotivated. Instead, start with one junk drawer, closet, or room at a time.

Appreciate the process and stay in the moment. Purging will teach you a lot about yourself, your needs, and your wants. Instead of being overwhelmed by future uses for an object or the meaning imbued in your things, ask yourself how it makes you feel right now. It may take you multiple passes at purging in order to actually make any headway in downsizing, but trust that each pass will bring you closer to that simple life of your dreams.

Practice gratitude. You might have a lot of things and that can be overwhelming. One way to get over what seems like an enormous task at hand? Focus on how lucky you are to have had a bounty, and how fortunate you are to be able to give things away.

https://www.nextavenue.org/have-difficult-conversations-with-your-aging-parents/?hide_newsletter=true&utm_source=Next+Avenue+Email+Newsletter&utm_campaign=e79fedc9a9-09.25.2018_Tuesday_Newsletter&utm_medium=email&utm_term=0_056a405b5a-e79fedc9a9-164951325&mc_cid=e79fedc9a9&mc_eid=dc856db226