If you’re on the fence about whether or not you want to sell your house this year, there’s good news. For nearly two years, real estate professionals have worked tirelessly to ensure the safety of buyers and sellers during the pandemic.

Today, they’re seasoned experts, not just in the art of buying and selling homes, but also in how to keep you safe throughout the process. Real estate professionals have learned new technologies plus safety and sanitation measures. As new variants emerge, those lessons continue to be key ways agents add value.

Real Estate Advisors Stay Current on Guidance for In-Person Showings

Agents don’t leave your health up to chance. They follow guidance from the Centers for Disease Control (CDC) and the National Association of Realtors (NAR) to ensure in-person showings are safe. NAR maintains industry-specific resources to ensure agents are informed on the latest recommendations and best practices.

Guidance from the CDC also equips real estate professionals with the know-how to employ sanitization and disinfectant measures during the health crisis, so they’re safe for you and your potential buyers.

Digital Tools Can Enhance Your Home Sale

In addition, agents are also well versed in using technology and digital tools to sell your home efficiently. In their guidance for realtors, NAR says:

“The COVID-19 pandemic is impacting members in unprecedented ways, and raises numerous unique and novel issues for the real estate industry.”

Real estate advisors have responded by reimagining the tech and tools they use. For instance, serving clients at a distance and limiting exposure to others is more important now than ever. That’s because restricting the number of people you need to interact with during the sales process is one of the best ways to keep everyone safe.

To accomplish this, agents now use a variety of methods to serve their clients, including:

Virtual Open Houses, Tours, and Listing Appointments

High-Quality Photos for Websites and Social Media

eSignature

Video Conferencing

Bottom Line

The health challenges we face today have fundamentally changed the way real estate professionals conduct business for the better. Let’s connect today so you have the latest tools on your side to feel safe and confident when you sell your house this year.

Many homeowners who plan to sell in 2022 may think the wise thing to do is to wait for the spring buying market since historically about 40 percent of home sales occur between April and July. However, this year’s expected to be much different than the norm. Here are five reasons to list your house now rather than waiting until the spring.

1. Buyers Are Looking Right Now, and They’re Ready To Purchase

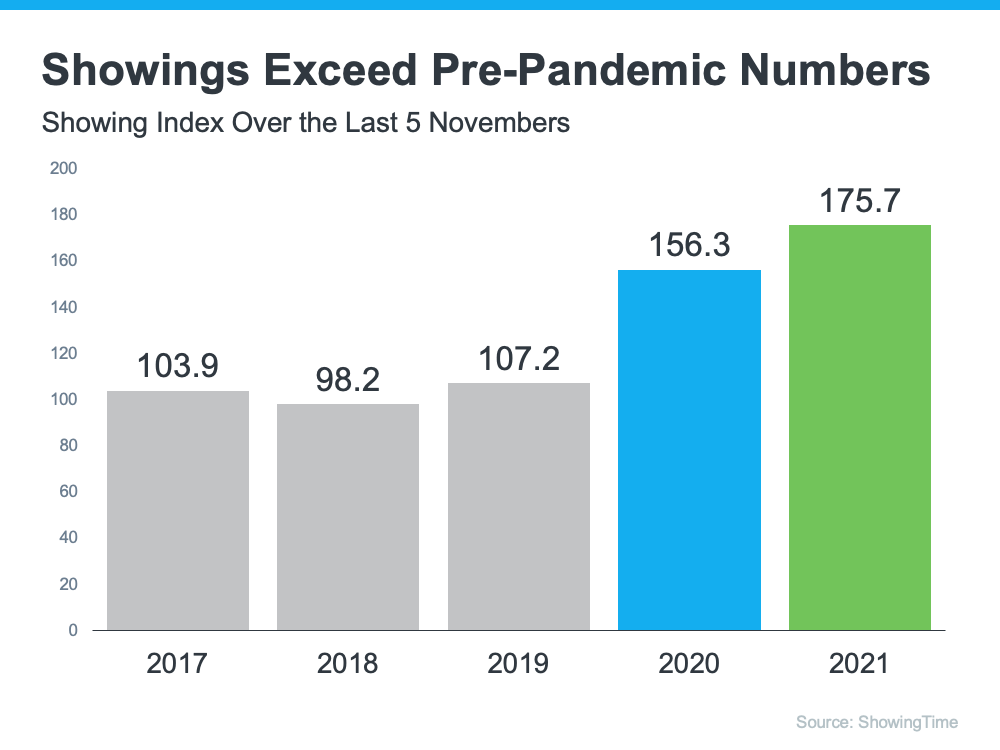

The ShowingTime Showing Index reports data from more than six million property showings scheduled across the country each month. In other words, it’s a gauge of how many buyers are out looking at homes at the current time.

The latest index, which covers November showings, reveals that buyers are still very active in the market. Comparing this November’s numbers to previous years, this graph shows that the index is higher than last year and much higher than the three years prior to the pandemic. Clearly, there’s an influx of buyers searching for your home.

Also, at this time of year, only those purchasers who are serious about buying a home will be in the market. You and your loved ones won’t be inconvenienced by casual searchers. Freddie Mac addresses this in a recent blog:

“The buyers who are willing to house hunt in a winter market, when there are fewer options, are typically more serious. Plus, year-end bonuses and overtime payouts give people more purchasing power.”

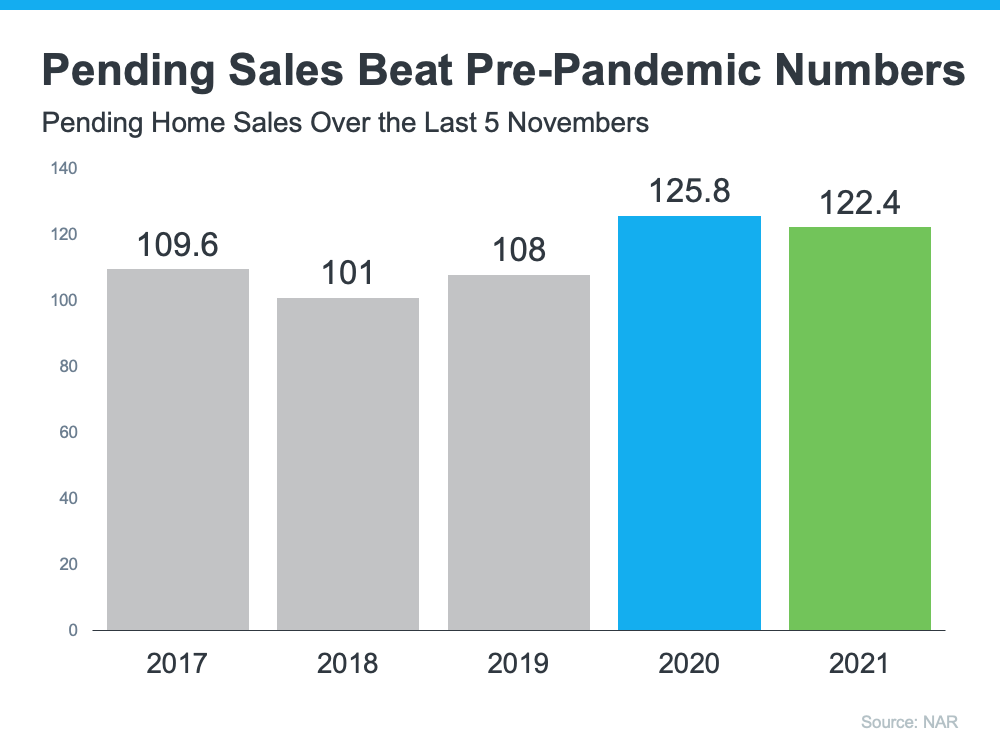

And that theory is proving to be true right now based on the number of buyers who have put a home under contract to purchase. The National Association of Realtors (NAR) publishes a monthly Pending Home Sales Index which measures housing contract activity. It’s based on signed real estate contracts for existing single-family homes, condos, and co-ops. The latest index shows:

“…housing demand continues to be high. . . . Homes placed on the market for sale go from ‘listed status’ to ‘under contract’ in approximately 18 days.”

Comparing the index to previous Novembers, while it’s slightly below November 2020 (when sales were pushed to later in the year because of the pandemic), it’s well above the previous three years.

The takeaway for you: There are purchasers in the market, and they’re ready and willing to buy.

2. Other Sellers Plan To List Earlier This Year

The law of supply and demand tells us that if you want the best price possible and to negotiate your ideal contract terms, put your house on the market when there’s strong demand and less competition.

A recent study by realtor.com reveals that, unlike in previous years, sellers plan to list their homes this winter instead of waiting until spring or summer. The study shows that 65% of sellers who plan to sell in 2022 have either already listed their home (19%) or are planning to put it on the market this winter.

Again, if you’re looking for the best price and the ability to best negotiate the other terms of the sale of your house, listing before this competition hits the market makes sense.

3. Newly Constructed Homes Will Be Your Competition in the Spring

In 2020, there were over 979,000 new single-family housing units authorized by building permits. Many of those homes have yet to be built because of labor shortages and supply chain bottlenecks brought on by the pandemic. They will, however, be completed in 2022. That will create additional competition when you sell your house. Beating these newly constructed homes to the market is something you should consider to ensure your house gets as much attention from interested buyers as possible.

4. There Will Never Be a Better Time To Move-Up

If you’re moving into a larger, more expensive home, consider doing it now. Prices are projected to appreciate by approximately 5% over the next 12 months. That means it will cost you more (both in down payment and mortgage payment) if you wait. You can also lock in your 30-year housing expense with a mortgage rate in the low 3’s right now. If you’re thinking of selling in 2022, you may want to do it now instead of waiting, as mortgage rates are forecast to rise throughout the year.

5. It May Be Time for You To Make a Change

Consider why you’re thinking of selling in the first place and determine whether it’s worth waiting. Is waiting more important than being closer to your loved ones now? Is waiting more important than your health? Is waiting more important than having the space you truly need?

Only you know the answers to those questions. Take time to think about your goals and priorities as we move into 2022 and consider what’s most important to act on now.

Bottom Line

If you’ve been debating whether or not to sell your house and are curious about market conditions in your area, let’s connect so you have expert advice on the best time to put your house on the market.

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

“The New Year is often a time for starting fresh, and whether your goals for the new year are inward or outward, this issue of American Lifestyle can help you set up yourself up for a successful year ahead.” Follow the link below to learn more!

As a buyer in a sellers’ market, sometimes it can feel like you’re stuck between a rock and a hard place. When you’re ready to make an offer on a home, remember these five easy tips to help you rise above the competition.

1. Know Your Budget

Knowing your budget and what you can afford is critical to your success as a homebuyer. The best way to understand your numbers is to work with a lender so you can get pre-approved for a loan. As Freddie Mac puts it:

“This pre-approval allows you to look for a home with greater confidence and demonstrates to the seller that you are a serious buyer.”

Showing sellers you’re serious can give you a competitive edge, and it helps you act quickly when you’ve found your perfect home.

2. Be Ready To Move Fast

Homes are selling quickly in today’s competitive housing market. According to the Existing Home Sales Reportfrom the National Association of Realtors (NAR):

“Eighty-three percent of homes sold in November 2021 were on the market for less than a month.”

When houses are selling this fast, staying on top of the market and moving quickly are key. Your agent can help you put together and submit your best offer as soon as you find the home you want to buy.

3. Lean on a Real Estate Professional

No matter what the housing market looks like, rely on a trusted real estate advisor. As Freddie Mac also notes:

“The success of your homebuying journey largely depends on the company you keep. . . . Be sure to select experienced, trusted professionals who will help you make informed decisions and avoid any pitfalls.”

Agents are experts in the local real estate market. They have insight into what’s worked for other buyers in your area and what sellers may be looking for in an offer. It may seem simple, but catering to what a seller needs can help your offer stand out.

4. Make a Strong, but Fair Offer

According to the latest Realtors Confidence Indexfrom NAR, 40% of offers today are above the list price. In such a competitive market, emotions and prices can run high. Having an agent to help you submit a strong, yet fair offer is critical in these situations. Your agent can help you understand the market value of the home and recent sales trends in the area.

5. Be a Flexible Negotiator

When putting together an offer, your trusted real estate advisor will help you consider which levers you can pull, including contract contingencies (conditions you set that the seller must meet for the purchase to be finalized). Of course, there are certain contingencies you don’t want to give up. Freddie Mac explains:

“Resist the temptation to waive the inspection contingency, especially in a hot market or if the home is being sold ‘as-is’, which means the seller won’t pay for repairs. Without an inspection contingency, you could be stuck with a contract on a house you can’t afford to fix.”

Bottom Line

Today’s competitive landscape makes it more important than ever to make a strong offer on a home. Let’s connect to make sure you rise to the top along the way.

Once you’ve found your dream home and applied for a mortgage, there are some key things to keep in mind before you close. It’s exciting to start thinking about moving in and decorating your new place, but before you make any large purchases, move your money around, or make any major life changes, be sure to consult your lender – someone who’s qualified to explain how your financial decisions may impact your home loan.

Here’s a list of things you shouldn’t do after applying for a mortgage. They’re all important to know – or simply just good reminders – for the process.

1. Don’t Deposit Cash into Your Bank Accounts Before Speaking with Your Bank or Lender.

Lenders need to source your money, and cash isn’t easily traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

2. Don’t Make Any Large Purchases Like a New Car or Furniture for Your Home.

New debt comes with new monthly obligations. New obligations create new qualifications. People with new debt have higher debt-to-income ratios. Since higher ratios make for riskier loans, qualified borrowers may end up no longer qualifying for their mortgage.

3. Don’t Co-Sign Other Loans for Anyone.

When you co-sign, you’re obligated. With that obligation comes higher debt-to-income ratios as well. Even if you promise you won’t be the one making the payments, your lender will have to count the payments against you.

4. Don’t Change Bank Accounts.

Remember, lenders need to source and track your assets. That task is much easier when there’s consistency among your accounts. Before you transfer any money, speak with your loan officer.

5. Don’t Apply for New Credit.

It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), your FICO® score will be impacted. Lower credit scores can determine your interest rate and possibly even your eligibility for approval.

6. Don’t Close Any Credit Accounts.

Many buyers believe having less available credit makes them less risky and more likely to be approved. This isn’t true. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those determinants of your score.

Bottom Line

Any blip in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. If your job or employment status has changed recently, share that with your lender as well. The best plan is to fully disclose and discuss your intentions with your loan officer before you do anything financial in nature.

What does the coming year hold for the housing market? Here’s what experts project for 2022.

Mortgage rates are projected to rise and so are home prices. Experts are forecasting buyer demand will remain strong as people try to capitalize on rates and prices before they climb, creating another strong year for home sales.

Let’s connect so you can make your best move in the new year.

It’s no secret that we love our furry friends – about 70% of U.S. households have pets. What may come as a surprise is how large a role they play in the homebuying process.

Americans spend $1,163 a year on their pets, and nearly half of pet owners say they would move for better accommodations and amenities for their pets.

If you’re thinking of adding a furry friend, or if you already have, let’s connect to discuss how you can find a home that meets all your pet’s needs.

Since the pandemic began, Americans have reevaluated the meaning of the word home. That’s led some renters to realize the many benefits of homeownership, including the feelings of security and stability and the financial benefits that come with rising home equity. At the same time, many current homeowners have decided their house no longer meets their needs, so they moved into homes with more space inside and out, including a home office for remote work.

However, not every purchaser has been able to fulfill their desire for a new home. Here are two obstacles some homebuyers are facing:

The ability to save for a down payment

The ability to qualify for a mortgage at the current lending standards

This past week, both of those challenges have been mitigated to some degree for many purchasers. The FHFA (which handles mortgages by Freddie Mac, Fannie Mae, and the Federal Housing Administration) is raising its loan limit for prospective purchasers in 2022. The term used to describe the maximum loan amount they will entertain is the Conforming Loan Limit.

What Is the Difference Between a Conforming Loan and a Non-Conforming Loan?

Investopedia explains the difference in a recent post:

“Conforming loans are the only loans that meet the requirements to be acquired by Fannie Mae and Freddie Mac. Jumbo loans, which exceed the conforming limit, are the most common type of nonconforming loan.”

What Difference Does It Make to Me as a Home Buyer?

A Forbesarticle earlier this year explains the benefits of a conforming loan and why they exist:

“Since lenders can’t sell non-conforming loans to Fannie Mae or Freddie Mac to free up their cash, they’re a bit riskier for the lender. This is especially true for jumbo loans, which aren’t backed by any government guarantees. If you default on a jumbo loan, it’s a huge blow to the lender.

Thus, lenders generally charge higher interest rates to compensate, and they can have even more requirements. For example, lenders who give out jumbo loans often require that you make a down payment of at least 20% and show that you have at least six months’ worth of cash in reserve, if not more.”

What Happened Last Week?

The FHFA has significantly increased its Conforming Loan Limits for 2022. Sandra L. Thompson, FHFA Acting Director, explains in the press release that:

“Compared to previous years, the 2022 Conforming Loan Limits represent a significant increase due to the historic house price appreciation over the last year. While 95 percent of U.S. counties will be subject to the new baseline limit of $647,200, approximately 100 counties will have conforming loan limits approaching $1 million.”

This means that more homes now qualify for a conforming loan with lower down payment requirements and easier lending standards – the two challenges holding many buyers back over the last year.

The Federal Housing Administration (FHA) also increased its Conforming Loan Limits for 2022. That could also mean an easier path to homeownership for many prospective buyers. As the Forbes article explains:

“FHA loans can be very beneficial if you don’t have as much savings, or if your credit score could use some work.”

Bottom Line

Buying your first or your next home may have just gotten much easier (less stringent qualifying standards) and less expensive (possibly lower mortgage rate). Let’s connect to discuss how these changes may impact you.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

![2022 Housing Market Forecast [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/12/15133953/20211217-MEM-1046x2117.png)

![A Happy Tail: Pets and the Homebuying Process [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/12/08135318/20211210-MEM-1046x1910.png)