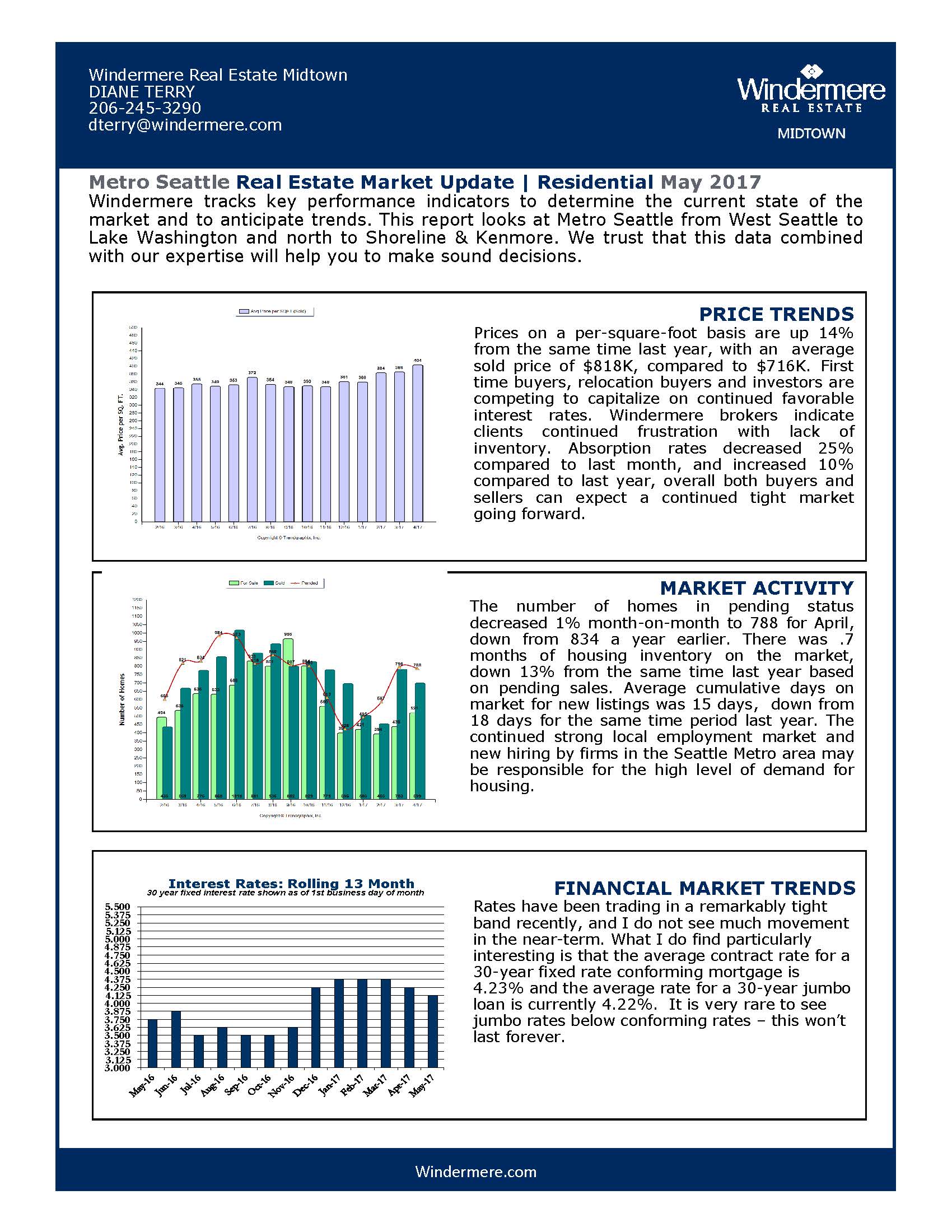

Buying a Home Prior to Marriage

One of the questions I am sure many kids ask their parents is should we buy a house before we’re married or wait to buy until after the wedding?

Buying a house before marriage is something that should be given a considerable amount of thought. A Coldwell Banker study found that quarter of younger couples – those between 18 and 34 – are buying a home before they get married.

If you and your partner are considering a home purchase, it is essential that you take appropriate steps to protect yourself during and after the purchase.

While it can feel “unromantic” to talk about finances, legal protections, and what you plan to do if things don’t work out, failing to be smart about the most significant financial purchase of your life can lead to significant regrets down the road.

In fact, without proper planning, you’ll probably increase the odds of needing to sell the home due to a breakup. Even though you are not married, you might have many of the same issues to deal with as if you were going through a divorce!

Preparing for a home purchase as an unmarried couple takes a little effort on your part, including some honest conversations and careful planning.

Considerations Before Buying as an Unmarried Couple

Current Finances

You and your partner need be completely clear about both of your financial situations. You are about to make a major purchase together, and like any business transaction, you need to know that your partner is capable of holding up his or her end of the bargain.

You and your partner need to share current, up-to-date information about your credit score, debt, income, and other financial obligations. All of this information is going to be required for getting a mortgage anyway, so it will all come out into the open before you can purchase the home.

One very important thing couples purchasing before marriage need to understand is debt obligations. When you both co-sign a mortgage together, each party is responsible for the complete debt. What does this mean in the real world? If you and your partner split and he or she decide not to pay the mortgage, you’ll be held responsible.

If things go sour, this can put you in a terrible spot. For this reason, many financial planners recommend not to buy a home for more than one person’s salary. If there is a breakup, you would still be able to afford the mortgage even if only for a short time. Again, this is where discussing finances before purchasing becomes very important.

Check out these mortgage tips for first-time buyers to be financially prepared for home ownership. You’ll also get some great advice by checking out these twenty things to do before buying a home.

Credit Scores

Your credit score and the score of your partner is a significant factor in your ability to get a mortgage. A higher credit score tends to ensure a better mortgage rate, which can save you tens of thousands of dollars over the life of the loan. Before you buy, you want to know exactly what both of your credit scores are.

As a married couple, your scores could be lumped together, but as an unmarried couple, they can be considered separately if necessary. You have the option of having the person with the better score apply for the mortgage, thus avoiding the drag of the lower credit score on the loan terms.

But keep in mind that when the person with the better score takes out the loan, it is only his or her income that is taken into account for the home purchase. The single income will need to be enough to pay the mortgage – which may or may not be a problem in your circumstances.

Remember credit scores play a significant role in getting the lowest mortgage interest rates. Make sure you analyze your current credit and try to improve your score before purchasing. Increasing your credit score could save you thousands of dollars over the life of the loan.

The three major credit reporting agencies are required to give one free credit report a year. As long as you haven’t requested a free report in the past year, you can go online and download your three free reports. You can go to the Annual credit report to get all three.

Future Finances

Money problems are one of the leading causes of relationship troubles, for married or unmarried couples. And few purchases can lead to money problems more easily than buying a home. You and your partner need to draft an agreement – on paper – that lays out who will pay for what, and how much. These include:

Down Payment

One of you may have a lot more money to put towards the down payment. Or you may put in equal amounts. However, you arrange the down payment, be clear about who is putting down how much, and what that means over the long-term – such as if you sell, or break up.

Mortgage Payments

How much will each of you pay toward the mortgage? Plenty of couples have unequal mortgage payment arrangements due to differences in income, but again, you need to discuss what that means concerning each of your equity over time. Not talking about financial issues like these can cause unwanted stress down the road.

Fees

There are a lot of other costs that come up beside the mortgage payment. For example, you may need to pay homeowners association fees. Depending on your down payment, you might need to pay mortgage insurance. Property taxes are another fee that can be pretty substantial in specific areas. Here are some additional expenses when buying a house you may not have given much thought to.

All of these items should be factored into your budget when buying a home, especially when you are not married.

Maintenance

One of the most significant costs of home ownership that new owners are not prepared for is maintenance and repairs. The water heater breaks, the stove stops working, the fridge goes out – you need money to pay for these things when they happen. Will both of you cover the costs equally? If not how will these kinds of expenses be divided?

Upgrades

Upgrades may come a few years down the line, but when they do, you want to know who will pay for them. Not long ago, I had unmarried clients who purchased a home in Southborough Massachusetts. It was clear to me they were not on the same page when it came their purchase. One of the parties was already planning the improvements, while the other was without question putting up a big STOP sign.

What Kind of Home You’re Going to Buy

When buying a home before marriage, it is essential to get on the same page about what you both want. This not only includes the house itself but these considerations as well:

- What kind of location – big city, little town or a home in the country?

- What kind of home – a re-sale, new construction, an antique, fixer upper?

- What price point – a frank discussion of where your comfort level lies. The mortgage broker may say you are qualified to purchase a lot more than one party is comfortable with.

- What kind of neighborhood – once the location is narrowed down, you’ll need to decide if you want a large subdivision, country road or busy street. One partner might have a strong preference for one or the other. See the guide on how to pick a neighborhood.

- What about schools – if you are planning on having kids together, the school system could become a major consideration.

- Is commute relevant to one or both parties – understanding location needs is important when buying a home together.

Remember you both need to be on the same page so that one party isn’t left feeling uncomfortable.

Open a Joint Bank Account

While you may not be married, opening up a joint bank account might be a prudent consideration for those who are buying a home before marriage. The joint account can be used to pay agreed upon bills pertaining to the house you’ve purchased.

Some financial experts agree you might want to automatically have a certain amount of money from individual accounts deposited monthly. By doing so, neither party forgets creating money arguments in the future on who paid what. Each side would have a set amount deposited each month into the joint account.

Title Options

You have several different types of title arrangements that you can choose from based on your situation. They include:

Joint Tenants in Common

In the joint tenants in common arrangement, you decide what percentage of the home each partner is responsible for. You can do a 50/50 split, but most people choose this option because it allows a different arrangement, like 60/40, and because you can designate who your share goes to when you pass away.

Either through your will, or through the probate process specific to your state, your percentage of the home will be distributed to your heirs/relatives/etc.

Joint Tenancy with Rights of Survivorship

With the joint tenancy arrangement, you and your partner own the home equally, 50/50. You also agree that your partner will get your share of the property should you pass away, and vice versa. This agreement mirrors the standard arrangement assumed when a married couple buys a home.

If you die, your half of the property automatically becomes your partner’s. In other words, there is no option to leave your equity to your parents, siblings, other relatives, or other heirs.

Sole Ownership

It is also possible for the home to belong entirely to just one partner. Although it is not as common, there may be reasons you choose to go with the sole ownership route – like if only one person is getting the mortgage on the home.

What Happens if it Doesn’t Work Out

Most people don’t like to plan for failure, but it is something worth considering when buying a home jointly before marriage. When relationships turn sour, things can get contentious. Here are some items to think about:

- If a break up does occur, who is going to stay in the home?

- What happens if neither of you can afford to pay the mortgage alone?

- Will the house be sold?

- Will one party purchase the home from the other?

- How will the purchase price be determined?

- What if you want to sell and your partner doesn’t?

- Who will be responsible for paying for a large unplanned expense like a heating system needing replacement?

- How will you pick the Realtor to use when splitting up?

As you can see owning a home out of wedlock brings with it some critical considerations. It is prudent that questions like these be addressed in a legal agreement.

Consider Getting a Legally Binding Agreement

While the title agreement is legally binding, the other decision you make together concerning finances are not – unless you take the proper steps to make it so. While it can seem overly technical and cynical to talk to a lawyer about your agreement, doing so will give you more peace of mind in the future.

Making your agreement legally binding means, you are both serious about doing what you say you will do. You can always change the deal if the situation changes. Talking with a lawyer before a big business/financial decision is still recommended.

Some of the most prominent disagreements can be avoided when you have an agreement in place to spell out each other’s obligations.

Full article via: www.maxrealestateexposure.com/buying-house-before-marriage/

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link